The Middle East conflict is being discussed as an oil and gas disruption. That framing misses the bigger shift.

This is an infrastructure stress test for the digital economy.

For over a decade, tech scaled on a quiet assumption: energy would be abundant, predictable, and cheap. That assumption no longer holds. And the cracks are starting to show across AI, semiconductors, and global supply chains.

AI Data Centers Are Where the Pressure Shows First

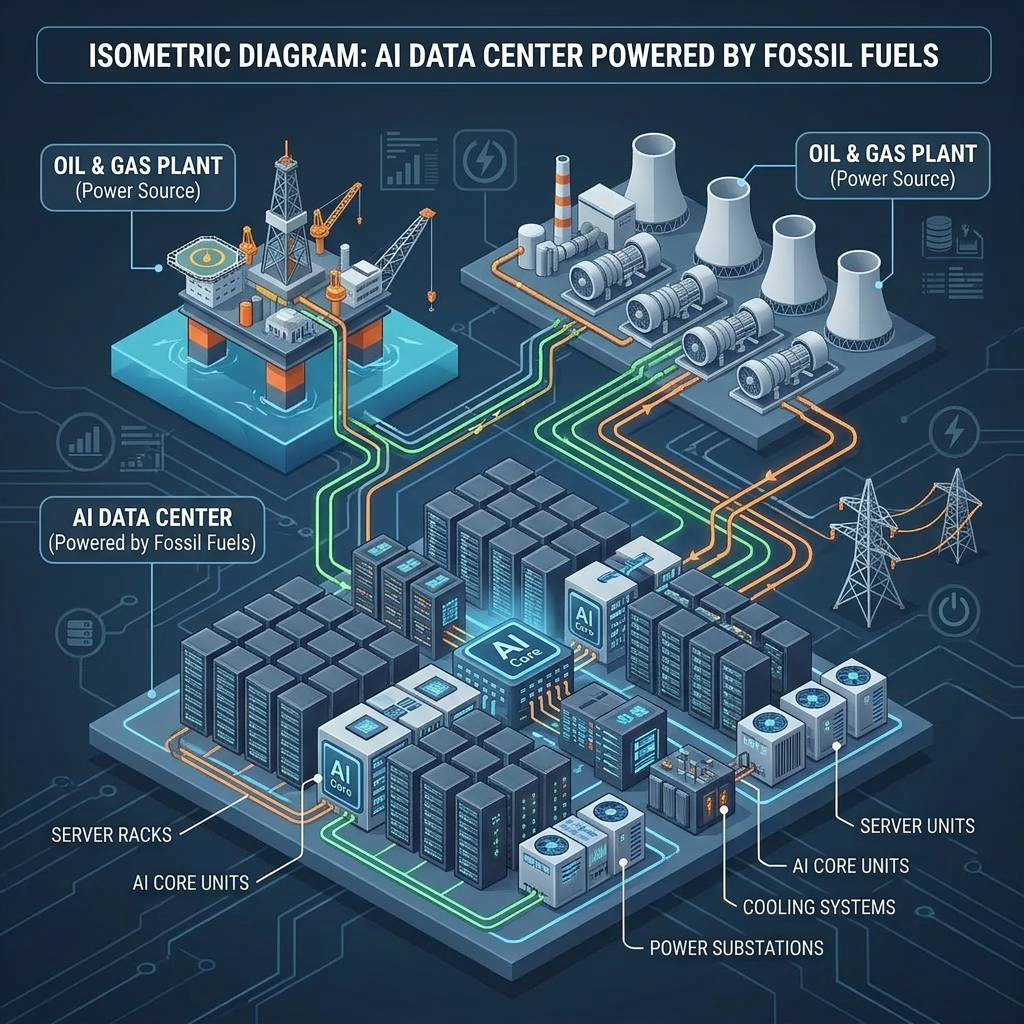

AI is not just compute-heavy. It is fundamentally energy-heavy.

Training large models can require 7–8x more energy than traditional workloads, with roughly half of that going into cooling dense GPU clusters. The International Energy Agency estimates that data centers already account for ~1–1.5% of global electricity demand, a figure expected to rise sharply with AI adoption.

At the same time, electricity in key markets remains heavily tied to natural gas. In the U.S., gas accounts for ~40% of power generation (U.S. Energy Information Administration).

When LNG supply tightens, AI infrastructure feels it almost immediately:

- Higher operating costs

- Slower capacity expansion

- Greater sensitivity to location

The implication is simple: AI scaling is now energy-constrained, not just compute-constrained.

Semiconductors Turn Energy into Cost, Instantly

On the supply side, semiconductors amplify the same problem.

A modern fabrication plant can consume electricity comparable to tens of thousands of households, running continuously with zero tolerance for disruption. Advanced processes like EUV lithography push that intensity even further.

According to industry estimates from organizations like SEMI, energy is one of the largest and fastest-growing components of fab operating costs.

This creates a direct link: higher energy prices → higher cost per wafer → pressure across the entire electronics value chain

At a time when governments are investing heavily in domestic chip capacity, energy is quietly becoming the gating factor for where fabs are economically viable.

Critical Materials: The Underestimated Bottleneck

Energy is only part of the equation. The more fragile layer sits in materials.

- Qatar supplies roughly 30–35% of global helium, essential for semiconductor manufacturing and cooling

- Israel and Jordan dominate global bromine production, used in electronics and chemical processes

- The Gulf region contributes around 10% of global aluminum supply, critical for EVs and hardware

These are not easily replaceable inputs. Disruptions don’t just increase prices. They create single-point failures in production systems.

Most supply chains are not designed for that level of concentration risk.

A Supply Chain That Runs on Oil

The modern tech supply chain is global by design and energy-dependent at every layer.

A single semiconductor can cross borders 70+ times and travel ~25,000 miles before final assembly. Meanwhile, core inputs like plastics, laminates, and specialty chemicals are derived from petrochemicals.

When oil prices rise:

- Input costs increase

- Freight becomes significantly more expensive

- Lead times become less predictable

This is not a linear effect. It compounds across the system.

What Leaders Need to Internalize Now

This is not a temporary spike. It is a structural shift.

First, energy is now a primary site selection variable. Not secondary. Not operational. Strategic.

Second, efficiency is becoming a margin lever. Incremental gains in power usage effectiveness (PUE), cooling, and workload optimization now translate directly into financial performance.

Third, supply chains must be designed for disruption, not efficiency alone. Multi-sourcing critical materials is no longer optional.

Finally, the economics of compute are changing. The assumption of cheap, abundant processing power is eroding. Pricing models will follow.

The Real Takeaway

The AI race is often framed around models, chips, and scale.

But the constraint is shifting.

The next phase of competition will be defined by access to energy and the ability to manage it intelligently.

That is not a technical problem. It is a strategic one.

And most organizations are not yet operating as if that’s true.